June 19, 2026

Strategic Energy Dependencies in an Interconnected World

Global commodity markets have entered a phase of unprecedented volatility as supply chain vulnerabilities expose the fragile foundations of international energy architecture. The Hormuz closure and global oil disruptions scenario represents a critical stress test for interconnected economies, where cascading effects ripple through manufacturing sectors, transportation networks, and financial systems worldwide.

Understanding these dependencies requires examining how energy-intensive industries have evolved to rely on specific fuel types and transportation corridors. Heavy oil derivatives, particularly diesel and jet fuel, have become critical inputs for agricultural production, logistics operations, and industrial manufacturing processes that form the backbone of global commerce.

When big ASX news breaks, our subscribers know first

The Strait's Role in Global Energy Infrastructure

Maritime energy chokepoints represent critical vulnerabilities in the global energy system. Recent market data indicates that approximately 21-25 million barrels per day of crude oil typically transit through major shipping lanes, with significant portions of global LNG shipments also dependent on these routes. The concentration of energy flows through limited geographic corridors creates systemic risks that extend far beyond immediate supply disruptions.

Energy infrastructure development has historically favoured centralised production and long-distance transportation networks. This model emerged during periods of abundant, low-cost energy resources, when the economic benefits of scale outweighed the risks of geographic concentration. However, changing market dynamics have begun to challenge these assumptions.

The economic foundation of current energy infrastructure reflects historical pricing patterns that may no longer be sustainable. Analysis of oil price rally insights shows that traditional cost structures have been disrupted by fundamental shifts in production economics and consumer affordability thresholds.

Pre-Closure Vulnerabilities in Maritime Energy Transport

Even before major disruptions, global energy markets exhibited signs of strain. World per capita diesel supply has been declining since the early 2020s, according to energy statistical reviews, indicating systemic supply constraints that predate current geopolitical tensions. This trend represents a critical vulnerability given diesel's essential role in heavy transportation, agricultural operations, and industrial processes.

The pricing dynamics for oil exporters reveal underlying structural problems. Historical analysis shows that during the 2011-2013 period, OPEC members required approximately $105 per barrel to balance fiscal budgets, while recent market prices have averaged only $65 per barrel. This 39% gap between producer requirements and market reality creates fundamental instability in global energy markets.

LNG transportation faces similar pressures. Furthermore, research indicates that only about 13% of natural gas is transported as LNG globally, making it an expensive and specialised method of energy transport. Middle Eastern LNG producers require prices in the $15-20 per million metric tons range, while major consuming nations like India resist paying more than $10 per unit, and coal replacement markets cannot support prices above $5 per unit.

These price mismatches create structural tensions that extend beyond temporary market fluctuations. The fundamental economics of energy production, transportation, and consumption have reached a critical inflection point where traditional market mechanisms struggle to balance producer needs with consumer capacity.

Historical Precedents of Energy Chokepoint Disruptions

Previous energy disruptions provide important context for understanding potential impacts. The 1973 Arab Oil Embargo demonstrated how rapidly energy supply constraints can cascade through global economies, triggering inflation, currency instability, and recession in major consuming nations. During that crisis, oil prices increased by more than 300% in a matter of months, fundamentally altering global economic relationships.

The Iran-Iraq War period from 1980-1988 offers particular relevance, as it involved sustained attacks on energy infrastructure and shipping in the Persian Gulf. During the "Tanker War" phase, more than 400 vessels were attacked, insurance costs skyrocketed, and alternative transportation routes experienced severe capacity constraints. Recovery of full production capacity required nearly five years after hostilities ended.

Moreover, more recent disruptions, including the 2019 attacks on Saudi Aramco facilities, demonstrated the vulnerability of modern energy infrastructure to precision targeting. These incidents temporarily reduced global oil supply by approximately 5%, triggering immediate price spikes and highlighting the limited spare capacity available to compensate for major production losses.

Economic research on historical energy disruptions reveals consistent patterns of demand destruction, supply chain reorganisation, and permanent shifts in energy consumption patterns. The stagflation period of the 1970s and early 1980s, lasting approximately 50-60 years according to economic cycle analysis, illustrates how energy constraints can trigger extended periods of economic restructuring.

Economic Sectors Under Greatest Pressure

Manufacturing Industries Dependent on Energy-Intensive Processes

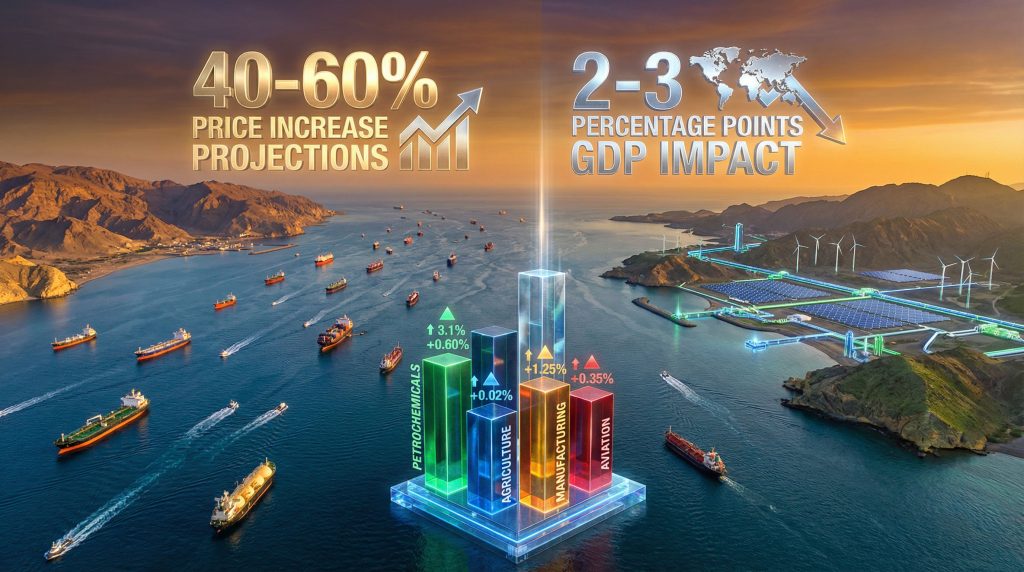

Manufacturing sectors face multiple layers of vulnerability during energy disruptions. Petrochemical production, which forms the foundation of plastics, synthetic materials, and chemical processing industries, requires both energy inputs and petrochemical feedstocks. The concentration of petrochemical production capacity in energy-producing regions creates supply chain dependencies that extend far beyond direct energy costs.

| Economic Sector | Direct Impact | Secondary Effects | Recovery Timeline |

|---|---|---|---|

| Petrochemicals | Supply shortage | Price volatility | 12-18 months |

| Agriculture | Fertiliser costs | Food price inflation | 6-12 months |

| Manufacturing | Energy costs | Production delays | 9-15 months |

| Aviation | Fuel availability | Route adjustments | 3-6 months |

Steel and aluminium production represent particularly energy-intensive industries vulnerable to supply disruptions. These sectors typically consume 10-15% of total industrial energy in major manufacturing economies, with aluminium smelting requiring approximately 14-16 MWh per ton of production. Energy costs can represent 30-40% of total production costs in these industries, making them extremely sensitive to price volatility.

Cement production, essential for construction and infrastructure development, faces similar vulnerabilities. The industry requires approximately 4 GJ of energy per ton of cement produced, with transportation fuel representing an additional cost component for raw material delivery and product distribution.

Manufacturing supply chains have evolved to optimise for efficiency rather than resilience. Just-in-time inventory systems, global sourcing strategies, and lean production models minimise costs under normal conditions but create cascading vulnerabilities when energy supplies face disruption.

Agricultural Supply Chains and Fertiliser Dependencies

Modern agricultural systems depend heavily on petroleum-derived inputs, creating vulnerabilities that extend directly to food security. Fertiliser production requires substantial natural gas inputs, with ammonia synthesis consuming approximately 28-30 GJ per metric ton of nitrogen fertiliser produced. Energy costs typically represent 60-80% of ammonia production costs, making agricultural inputs extremely sensitive to energy price volatility.

Transportation of agricultural products creates additional vulnerabilities. Heavy-duty trucks, which transport the majority of food products from farms to distribution centres, rely exclusively on diesel fuel. Agricultural logistics consume approximately 2% of total diesel production globally, but represent critical infrastructure for food security.

Food processing industries face dual pressures from energy costs and supply chain disruptions. Refrigeration, packaging, and processing operations require reliable energy supplies, while transportation constraints can disrupt the flow of raw materials and finished products.

In addition, the concentration of fertiliser production in energy-rich regions creates geographic vulnerabilities for global food systems. Approximately 60% of global ammonia capacity is located in regions that could face supply disruptions, potentially affecting agricultural productivity worldwide.

Transportation Networks and Logistics Bottlenecks

Transportation systems represent the circulatory system of modern economies, making them critical points of vulnerability during energy disruptions. Aviation fuel accounts for approximately 8-10% of global refined product demand, but its specialised nature and limited storage capacity create acute vulnerability to supply interruptions.

Maritime shipping, which handles approximately 90% of global trade by volume, faces constraints from both fuel availability and route accessibility. Container shipping typically consumes 300-400 tons of fuel per day for large vessels, with global shipping accounting for roughly 3% of global petroleum consumption.

Heavy-duty trucking represents another critical vulnerability. Long-haul freight transport consumes approximately 25% of total diesel production in major economies, making logistics networks highly sensitive to fuel supply disruptions or price increases.

Railway systems, while more fuel-efficient per ton-mile, still require substantial diesel inputs for freight operations. In major continental economies, rail freight consumes approximately 3-4 billion gallons of diesel annually, representing critical infrastructure for bulk commodity transport.

Financial Markets and Energy Trading Mechanisms

Energy trading markets have evolved into complex financial ecosystems that amplify the economic impacts of physical supply disruptions. Derivatives markets for crude oil, refined products, and natural gas trends represent trillions of dollars in notional value, creating leverage effects that can magnify price volatility.

The correlation between energy prices and broader financial markets has increased substantially over recent decades. Statistical analysis shows that energy price volatility now explains approximately 40-50% of commodity market variance and 15-20% of equity market volatility during crisis periods.

Currency markets face particular pressure during energy disruptions. Energy-importing nations typically experience currency depreciation as import costs rise, while energy exporters may see currency appreciation offset by economic disruption. These currency movements create additional inflationary pressures for energy-importing economies.

Financial institutions face direct exposure through energy sector lending and indirect exposure through economic slowdown effects. Energy sector loans typically represent 10-15% of commercial banking portfolios in major economies, creating potential financial stability concerns during extended energy crises.

Regional Economic Vulnerability Analysis

Asia-Pacific Economic Vulnerabilities

The Asia-Pacific region represents the world's largest energy-importing region, creating acute vulnerability to supply disruptions. China imports approximately 75% of its crude oil needs, with heavy dependence on Middle Eastern supplies. Industrial energy consumption in China accounts for approximately 65% of total energy demand, making manufacturing sectors particularly vulnerable to price volatility.

India's energy import dependency has reached approximately 87% for crude oil and 50% for natural gas, creating significant foreign exchange pressures during energy price spikes. The Indian economy's growth trajectory depends heavily on affordable energy inputs, with energy intensity remaining approximately 40% higher than OECD averages.

Japan and South Korea face particular vulnerability due to limited domestic energy resources and high industrial energy consumption. Japan imports approximately 99% of its oil and gas requirements, while South Korea imports 97% of its energy needs. Both economies have developed substantial strategic petroleum reserves, typically maintaining 150-200 days of import coverage.

Southeast Asian manufacturing hubs face disruptions to their role as global production centres. Countries like Vietnam, Thailand, and Malaysia have become integrated into global supply chains that depend on reliable energy supplies and transportation networks. Manufacturing sectors in these economies typically consume 30-40% of total energy demand.

European Market Adaptations and Alternatives

European economies have developed sophisticated energy security mechanisms following previous supply disruptions. Strategic petroleum reserves across EU member states total approximately 120 days of net imports, providing buffer capacity during short-term disruptions.

LNG infrastructure development has accelerated dramatically, with European LNG import capacity increasing by approximately 50% since 2020. Floating storage and regasification units provide flexible capacity that can respond rapidly to supply disruptions.

Pipeline diversification efforts have reduced dependence on single supply sources. Alternative pipeline capacity from Norway, Algeria, and Azerbaijan provides approximately 40% of European gas imports, reducing vulnerability to single-point failures.

Industrial demand response programmes have been developed to manage energy consumption during supply constraints. Large industrial consumers can typically reduce energy demand by 10-20% during emergency situations through process modifications and production scheduling changes.

North American Energy Market Responses

North American energy markets benefit from substantial domestic production capacity and integrated transportation networks. The United States has achieved approximate energy independence in crude oil production, with domestic production meeting roughly 95% of consumption requirements.

Canadian energy resources provide strategic depth for North American markets. Oil sands production capacity of approximately 3.5 million barrels per day and substantial natural gas reserves create buffer capacity during global supply disruptions.

Continental energy integration through pipeline networks provides resilience against external supply shocks. The North American pipeline system can transport approximately 25 million barrels per day of crude oil and refined products across the continent.

Refining capacity in the Gulf Coast region provides flexibility to process various crude oil grades and export refined products to global markets. Gulf Coast refineries process approximately 9 million barrels per day, representing crucial infrastructure for global energy markets.

Oil Price Dynamics and Market Evolution

Short-Term Market Shock Mechanisms

Energy market disruptions trigger immediate price discovery mechanisms that can create extreme volatility. Historical analysis indicates that major supply disruptions typically produce initial price increases of 40-60% within the first week of disruption onset. Financial markets amplify these moves through algorithmic trading and leverage effects.

Strategic petroleum reserve releases represent the primary policy tool for managing short-term price spikes. Coordinated releases from major consuming nations can provide approximately 60-90 days of additional supply, though this represents a limited and finite resource.

Speculative trading activities can substantially amplify price movements during crisis periods. Commodity futures markets typically see volume increases of 200-300% during major disruptions, with speculative positioning contributing to price volatility.

Furthermore, understanding OPEC market influence becomes crucial during such periods, as the organisation's response to supply disruptions can significantly impact global price dynamics.

Market intervention mechanisms include coordinated central bank actions, emergency lending facilities, and regulatory modifications to trading rules. These interventions can temporarily moderate price volatility but cannot address fundamental supply constraints.

Medium-Term Structural Adjustments

Extended supply disruptions trigger structural adjustments in energy consumption patterns and alternative supply development. Demand destruction typically begins when energy costs exceed 5-7% of household income or 15-20% of manufacturing costs for extended periods.

Alternative supply routes require substantial time and investment to develop. Pipeline projects typically require 3-5 years for completion, while LNG infrastructure development requires 4-7 years from conception to operation.

Investment flows redirect toward non-affected production regions during extended crises. Historical analysis shows that energy investment can shift by 30-50% between regions within 18 months of major supply disruptions.

Industrial adaptation includes energy efficiency improvements, fuel switching, and process modifications. Manufacturing sectors can typically achieve 10-15% energy intensity reductions within 12-18 months through operational changes.

Long-Term Economic Rebalancing Effects

Permanent changes to global energy trade flows emerge from extended disruptions. Regional energy security becomes a higher priority than global cost optimisation, leading to fundamental shifts in investment patterns and supply chain design.

Geopolitical risk premiums become embedded in long-term energy pricing. Markets begin to price reliability and security alongside cost, typically adding $10-15 per barrel in risk premiums for supplies from unstable regions.

The implications of Hormuz closure and global oil disruptions extend to accelerating energy transition investments. Renewable energy investment flows typically increase by 40-60% following major fossil fuel supply disruptions, as security concerns reinforce environmental motivations.

Economic relationships restructure around energy security considerations. Trade agreements, investment partnerships, and diplomatic relationships increasingly reflect energy supply considerations rather than pure economic efficiency.

Alternative Energy Infrastructure Development

Pipeline Network Expansion Opportunities

Pipeline infrastructure development represents the most cost-effective method for large-scale energy transport over land. Trans-Arabian pipeline capacity could potentially be expanded by 2-3 million barrels per day with substantial investment, though construction timelines typically require 4-6 years.

Central Asian energy corridors offer alternative routes for natural gas supplies. The Trans-Caspian pipeline system could potentially transport 30-40 billion cubic metres of natural gas annually to European markets, reducing dependence on traditional supply routes.

African energy export routes present long-term alternatives for both oil and gas supplies. West African pipeline capacity could be expanded to transport 1-2 million barrels per day additional crude oil production to global markets.

Pipeline economics depend heavily on utilisation rates and long-term supply commitments. Projects typically require 15-20 year purchase agreements to justify the substantial capital investments required.

Maritime Route Diversification Strategies

Cape of Good Hope routing represents the primary alternative for crude oil transportation, though it adds approximately 2-3 weeks to shipping times and increases transportation costs by $2-4 per barrel. Port infrastructure limitations in South Africa constrain the capacity for dramatically increased traffic.

Suez Canal alternative routing through Mediterranean ports could handle increased volumes, though capacity constraints limit throughput to approximately 120 ships per day compared to normal traffic levels of 50-60 ships daily.

Arctic shipping routes offer seasonal alternatives for energy transport, though ice conditions limit operations to 4-5 months annually. Climate change may gradually extend the operational season, but infrastructure limitations currently constrain cargo capacity.

Additional port capacity development requires substantial investment and time. New deep-water terminals typically require 3-5 years for construction and can cost $2-4 billion for facilities capable of handling large tankers.

Technological Innovation Acceleration

Floating storage and regasification units provide flexible LNG import capacity that can be deployed rapidly. Current global FSRU capacity totals approximately 150 billion cubic metres annually, with additional units requiring 12-18 months for construction and deployment.

Enhanced oil recovery technologies can increase production from existing fields. Advanced recovery methods can typically increase field recovery rates from 30-40% to 50-60% of original oil in place, though implementation requires 2-4 years and substantial investment.

Renewable energy infrastructure prioritisation accelerates during fossil fuel crises. Solar and wind capacity additions can typically be completed within 12-24 months, compared to 5-10 years for conventional power generation capacity, supporting energy security transition goals.

Energy storage technologies become critical for managing renewable energy intermittency. Battery storage costs have declined by approximately 80% over the past decade, enabling large-scale deployment to support renewable energy expansion.

The next major ASX story will hit our subscribers first

Central Bank Monetary Policy Responses

Interest Rate Policy Dilemmas

Energy-driven inflation creates complex challenges for monetary policymakers. Traditional inflation-fighting measures through interest rate increases can exacerbate economic slowdowns caused by energy supply constraints, creating a policy dilemma between price stability and economic growth.

Regional central bank coordination becomes essential during global energy crises. Coordinated interest rate policies can prevent competitive devaluations and capital flow disruptions that amplify energy crisis impacts.

Unconventional monetary policy tools may become necessary when traditional measures prove insufficient. Quantitative easing programmes, emergency lending facilities, and direct market interventions can provide liquidity during energy-driven financial stress.

Forward guidance becomes particularly important during energy crises as markets seek clarity on policy responses. Clear communication about monetary policy intentions can reduce uncertainty and moderate excessive market volatility.

Currency Market Implications

Energy supply disruptions create substantial pressures in currency markets. Energy-importing nations typically experience currency depreciation as import costs rise and current account balances deteriorate. The magnitude of currency movements can exceed 20-30% during severe energy crises.

Petrodollar system stability faces testing during major energy disruptions. The historical requirement for oil purchases in US dollars has provided structural support for dollar demand, though recent shifts toward alternative payment mechanisms could affect this relationship.

Safe haven asset reallocations accelerate during energy crises. Gold prices typically increase by 30-50% during major energy supply disruptions as investors seek inflation hedges and store of value assets.

Emerging market currencies face particular vulnerability due to limited foreign exchange reserves and higher energy import dependencies. Currency crises in energy-importing developing nations can create broader financial contagion effects.

Financial Stability Considerations

Banking sector exposure to energy-related loans creates potential stability risks. Energy sector loans typically represent 10-15% of commercial bank portfolios in major economies, with potential for significant losses during extended energy crises.

Insurance market capacity for energy disruptions faces strain during major events. Marine insurance, political risk insurance, and business interruption coverage can experience substantial claims that test industry capital adequacy.

Sovereign debt sustainability comes under pressure in energy-dependent nations. Countries with high energy import dependencies may see debt-to-GDP ratios deteriorate rapidly as economic growth slows and import costs rise.

Systemic risk monitoring becomes crucial as energy crises can trigger cascading failures across financial markets. Central banks must monitor interconnections between energy markets, commodity trading, and broader financial stability.

Policy Tools for Crisis Mitigation

Fiscal Policy Response Mechanisms

Strategic subsidy programmes for critical industries can maintain economic activity during energy supply constraints. Targeted support for transportation, agriculture, and manufacturing sectors can prevent widespread economic disruption while minimising fiscal costs.

Emergency energy assistance programmes help protect vulnerable populations from energy price increases. Household energy subsidies typically cost 1-2% of GDP during major energy crises but provide essential social stability during difficult periods.

Infrastructure investment acceleration can reduce long-term vulnerabilities while providing economic stimulus. Fast-track approval processes for energy infrastructure projects can reduce development timelines by 30-50%.

Strategic reserve management becomes crucial for maintaining supply security. Optimal release strategies must balance immediate price relief against maintaining sufficient reserves for extended disruptions.

International Coordination Frameworks

Multilateral energy security agreements provide frameworks for coordinated responses to supply disruptions. According to research on energy security measures, the International Energy Agency coordinating mechanism can organise releases of 150-200 million barrels from member country strategic reserves.

Emergency reserve sharing protocols enable mutual support during regional supply constraints. Bilateral and multilateral agreements can provide 30-60 days of additional supply during localised disruptions.

Trade policy adjustments facilitate energy alternative development. Temporary tariff reductions, expedited permitting, and regulatory flexibility can accelerate deployment of alternative energy supplies.

Diplomatic engagement remains essential for resolving underlying supply disruptions. Energy diplomacy requires balancing security concerns with economic relationships and long-term supply security.

Market Intervention Strategies

Price stabilisation mechanisms can moderate excessive volatility while preserving market signals. Strategic reserve releases coordinated with market timing can maximise impact while minimising reserves depletion.

Supply chain resilience investment incentives encourage private sector adaptation. Tax credits, loan guarantees, and regulatory streamlining can accelerate development of alternative supply sources.

Energy efficiency mandate acceleration reduces demand pressure during supply constraints. Building codes, vehicle efficiency standards, and industrial efficiency requirements can reduce energy demand by 5-10% over 2-3 years.

Market regulation adjustments may be necessary during extreme volatility. Position limits, margin requirements, and trading circuit breakers can prevent excessive speculation while maintaining market function.

Long-Term Structural Economic Changes

Supply Chain Regionalisation Trends

Near-shoring manufacturing investment patterns reflect growing prioritisation of supply chain resilience over cost optimisation. Manufacturing investment flows show increasing concentration within regional economic blocs rather than global optimisation strategies.

Regional energy security bloc formation creates new economic relationships based on energy supply stability. Trade agreements increasingly include energy security provisions that prioritise reliability over purely economic considerations.

Reduced global economic integration represents a fundamental shift from decades of increasing globalisation. Energy security concerns drive policy decisions that favour regional suppliers even when global alternatives offer lower costs.

Transportation cost increases from alternative routing make local production more competitive. When energy transport costs rise by 50-100%, the economics of global supply chains shift substantially toward regional alternatives.

Energy Security as Economic Policy Priority

National energy independence investment strategies receive unprecedented political and financial support. Energy security considerations override traditional cost-benefit analysis in infrastructure investment decisions.

Critical mineral supply chain diversification becomes essential for energy transition technologies. Lithium, cobalt, and rare earth mineral supply security receives strategic priority equal to traditional energy resources.

Renewable energy transition acceleration occurs not only for environmental reasons but for energy security benefits. Domestic renewable resources provide supply security that fossil fuel imports cannot match.

Energy storage deployment becomes a national security priority. Grid-scale battery storage, pumped hydro, and other storage technologies receive strategic investment support to enhance energy independence.

Geopolitical Economic Realignment

Middle East economic influence gradually diminishes as alternative energy sources gain prominence. Oil export revenues that historically provided geopolitical leverage decrease in relative importance.

Alternative energy producer nations gain increased economic and political influence. Countries with substantial renewable energy resources, critical minerals, or alternative fossil fuel supplies gain strategic importance.

New international economic partnership formations emerge based on energy complementarity rather than traditional trade relationships. Energy security alliances create new patterns of economic cooperation and investment.

Technology transfer accelerates as energy security concerns drive international cooperation in alternative energy development. Knowledge sharing agreements become strategic tools for energy security enhancement.

Navigating Economic Transformation Through Energy Disruption

Building Resilient Economic Frameworks

Economic resilience requires fundamental restructuring of energy-dependent systems. Diversification of energy sources, transportation routes, and supply chains becomes essential for maintaining economic stability during future disruptions.

Investment strategies must balance efficiency with resilience considerations. The historical focus on cost optimisation gives way to risk-adjusted decision making that considers supply chain vulnerabilities and geopolitical risks.

Institutional frameworks for crisis management require enhancement. Early warning systems, coordinated response mechanisms, and emergency authorities need strengthening to manage future energy supply disruptions effectively.

Private sector adaptation strategies include increased inventory management, supplier diversification, and alternative energy adoption. Companies must build flexibility into operations to manage energy supply variability.

Balancing Energy Security with Economic Efficiency

Policy frameworks must integrate energy security considerations with economic growth objectives. Traditional economic efficiency measures require modification to account for supply security and resilience factors.

Market mechanisms need adaptation to price supply security appropriately. Energy markets must develop pricing mechanisms that reflect not only current supply and demand but also reliability and security characteristics.

International cooperation remains essential despite increasing regionalisation trends. Global challenges require coordinated responses even as supply chains become more regionalised.

Furthermore, analysis of US-China trade impacts reveals how geopolitical tensions affect global energy security arrangements and economic cooperation frameworks.

Preparing for Permanent Global Economic Restructuring

Workforce adaptation programmes must prepare workers for changing energy sector employment patterns. Transition support, retraining programmes, and new skill development become essential for managing structural economic changes.

Financial system adaptation requires new risk management approaches. Banks, insurers, and investors must develop frameworks for managing energy transition risks and opportunities.

Regulatory frameworks require updating to address new energy security realities. Environmental regulations, safety standards, and market rules need revision to support energy security objectives.

Social safety net enhancements become necessary as energy transitions create economic disruptions. Support systems must help manage the social costs of economic restructuring while maintaining political stability.

The global economy stands at a critical juncture where energy supply disruptions catalyse fundamental structural changes. While short-term disruptions create significant challenges, they also accelerate necessary adaptations toward more resilient and sustainable economic systems. Success in navigating this transformation depends on coordinated policy responses, strategic investment decisions, and institutional adaptations that balance immediate crisis management with long-term structural resilience.

A Hormuz Strait closure would trigger immediate oil price increases of 40-60%, reduce global GDP growth by 2-3 percentage points, and accelerate permanent shifts toward regional energy security arrangements, fundamentally reshaping international economic relationships.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Energy market conditions can change rapidly, and readers should consult qualified financial advisors before making investment decisions. Historical performance does not guarantee future results, and energy market investments carry substantial risks including total loss of capital.

Want to Capitalise on Energy Market Volatility?

Whilst global energy disruptions create substantial market volatility, they also generate exceptional opportunities for informed investors. Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, including critical energy commodities that become increasingly valuable during supply chain disruptions. Begin your 14-day free trial today to position yourself ahead of market-moving energy and commodity discoveries.